The House of Lords has an Economic Affairs Committee (EAC) which has regular inquiries into economic matters that they think will be important for members of the House of Lords to understand. The structure of these inquiries is that the committee will hold a series of meetings to which it calls expert witnesses and asks them questions. A report will be produced at the end of the inquiry summarising what has been learned. Towards the end of 2023 they launched an inquiry with the title “How sustainable is our national debt.” The EAC announced the inquiry with the following words:

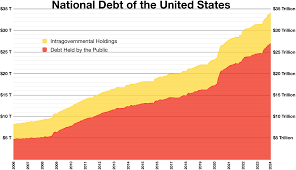

“How sustainable is our national debt? UK public sector net debt, often referred to as ‘national debt’, currently stands at just under 100 per cent of GDP. The UK’s growth outlook remains weak; quantitative easing has significantly increased the sensitivity of the UK’s debt to changes in short-term interest rates; and it is unclear whether the Government’s fiscal rule, as it relates to the national debt, is fit for purpose. The committee’s inquiry will investigate whether the UK’s national debt is on a sustainable path; if not, what steps are required; and whether the Government’s fiscal rule regarding the national debt is meaningful.”

For the debt/GDP ratio to fall either debt must fall and/or GDP must increase. How might GDP rise was one of the matters raised at a meeting on 13 February 2024 at which the witnesses were Carl Emmerson (Deputy Director at Institute of Fiscal Studies), Peder Beck-Friis (Senior Vice President and Economist at PIMCO), Sonja Gibbs (Head of Sustainable Finance at Institute of International Finance). We present part of the exchange between the witnesses and the members of the House of Lords below on the possibility of GDP growth through productivity growth.

Baroness Liddell of Coatdyke: I want to be a bit more specific. Carl, almost in your first sentence you talked about low-productivity growth, and it keeps coming up in the course of our discussions. How significant is it that the productivity puzzle needs to be solved? Do you have recommendations? A couple of weeks ago, we had Professor El-Erian with us, and his idea was to create a productivity tsar. He did not go into details as to what the tsar would be doing, but we have to concentrate on the practical outcomes that can deal with this productivity growth slowdown, which some studies have said is worse than it has ever been in over two decades. Give us some good ideas, please.

Carl Emmerson: The productivity slowdown has been phenomenal. In a counterfactual world where productivity growth had continued growing at the same rate as it had done between 1948 and 2007, we would all be sitting here in a country that was much more prosperous. Although we would have economic challenges, they would all seem much easier. It has been an absolutely dismal period for productivity growth. In the long run, that is the real driver of living standards. It is a huge public policy challenge.

I actually quite like the idea that we need institutional reform that gets us a focus on productivity across the board, because we know it is about policies in a load of different areas. Plus, we need a Government who are going to be patient, because it is sustainable growth that we want. I would quite like it if the idea was something we can do institutionally, which tries to keep the whole of government focused on what we can do to improve productivity. That could be a good step forward.

Baroness Liddell of Coatdyke: Can you focus it on long-term debt sustainability and match the two up?

Carl Emmerson: The idea here would be that, if we achieved greater productivity growth, it would make those economic trade-offs easier. It would make policy reform in a whole load of government areas easier, because you would have revenues to compensate losers. It could help cause a feedback loop, not the doom loop we were talking about earlier but a positive feedback loop. As we have been saying, the nicest way of getting debt to GDP down is to have higher growth relative to the interest rate you are paying on that debt.

Peder Beck-Friis: To add to the last point, and as I have said a few times, it is not growth in isolation that matters for debt sustainability; it is the interest rate/growth differential. Interest rates long term, structurally, tend to co-move pretty strongly with GDP growth rates. Productivity growth has been falling since the 1980s and so have interest rates. If we were to move into a world where, for instance, we boosted productivity growth, it may also lead to higher interest rates, in which case it is not obvious to me that it would have a beneficial impact on debt sustainability.

The Chair: I hear what you are saying, and I do not want to create an argument here. I was just reading what David Miles sent us from the OBR. He said, “If productivity growth is barely positive over the next five years debt would be around £200 billion higher, some 7% of GDP, than the OBR central forecast of November 2023”, which is an astounding figure. Does this not answer Lord Turnbull’s point that we really should be zeroing in on productivity rather than on the other side of the equation of just bringing debt down? It does strike me, reading that sentence.

Carl Emmerson: Where higher productivity growth can help is that it will make it easier for us to run a better primary balance than it otherwise would be.

Sonja Gibbs: What is interesting about the situation for the UK, as well as for many other countries, is that it is not about industrial structure; it is really a lack of capital investment and investment in skills. You get to that question of trade-off. If you increase spending on incentives for investment in strategic industries—things that are going to be very important going forward—and if you spend more on skills training, the impact of that spending on the debt should be offset by significantly higher growth. It is that balance that is important to achieve.

The Chair: Can I quickly pick up on immigration? We have not really talked about that. The OBR and the ONS are forecasting really quite high levels of migration through the forecast period. Again, it was striking what David Miles said in his written evidence. He points out the benefits of that and then goes on to say, “It is much less clear that persistently high levels of net immigration to boost the labour force can generate sustained fiscal improvements. New immigrants … may generate a favourable balance of extra tax revenue relative to extra public spending for some years. But immigrants who stay grow older and have children so the favourable tax to spending balance does not persist”.

Looking ahead, given the projections, is there a danger that we are looking towards growth being fuelled, in part at least or maybe too greatly, by these high levels of migration? Carl, what do you think about that?

Carl Emmerson: If we have more immigrants arriving in the UK, it is pretty clear that that boosts tax revenues. Many of them will be working; they will be spending in the economy. The way in which it often strengthens the public finances is that, when this occurs, we do not increase public service spending. Essentially, we have the same amount of public service spending going across a bigger population. Clearly, people arriving in the UK are bound to put some demand on some public services. Essentially, you achieve a stronger fiscal position because you have put a squeeze on public service spending and cut public spending per capita in a slightly subtle way.

Over the longer term, what happens is that, if people have children here and retire here, they will start to look much more like the population that is already here, and the public finances will not be much changed. If somebody arrives from overseas, stays here for a period and works for a bit, they may have a higher chance of retiring elsewhere in the world than somebody who is born here, who perhaps has a lower chance of retiring elsewhere. You might get a public finance win then.

The full transcript of this discussion can be found here:

https://committees.parliament.uk/event/20681/formal-meeting-oral-evidence-session